Household structure

Members, ownership splits, tax context, and SMSF settings sit in one place before any projection begins.

Track the household once. Then inspect cashflow, tax, suburb context, and retirement outcomes without rebuilding the spreadsheet.

Members, living expenses, loans, properties, and ownership stay connected, so every downstream view starts from the same facts.

Members, ownership splits, tax context, and SMSF settings sit in one place before any projection begins.

Properties, linked loans, rent, costs, depreciation inputs, and capital improvements stay tied to the same record.

Living expenses, income, repayments, and property cashflow read together before you change any forward assumptions.

Tax, cashflow, suburb research, retirement, and scenario views all reuse the same source model instead of forcing re-entry.

The public site should lead with the real decisions, because that is how the product is built internally too.

Compare holding value against sale proceeds, debt clearance, reinvestment, and CGT treatment in one path.

Inspect repayment change, cost drag, principal speed, and after-tax outcome before touching the loan.

Read retirement readiness, pathway comparisons, sale ledgers, and spendable-property outcomes from the current household model.

Stress household income, rent, and costs, then see how long cash survives and whether a forced sale appears.

Record the facts, read the current position, then pressure-test the next move.

Create the portfolio shell, then add members, properties, loans, ownership, and household spend without splitting the model across tools.

Review current cashflow, property tax, debt load, market context, and coverage before testing any new assumption.

Run retirement, sale, refinance, renovation, granny-flat, short-stay, and stress views against the same facts.

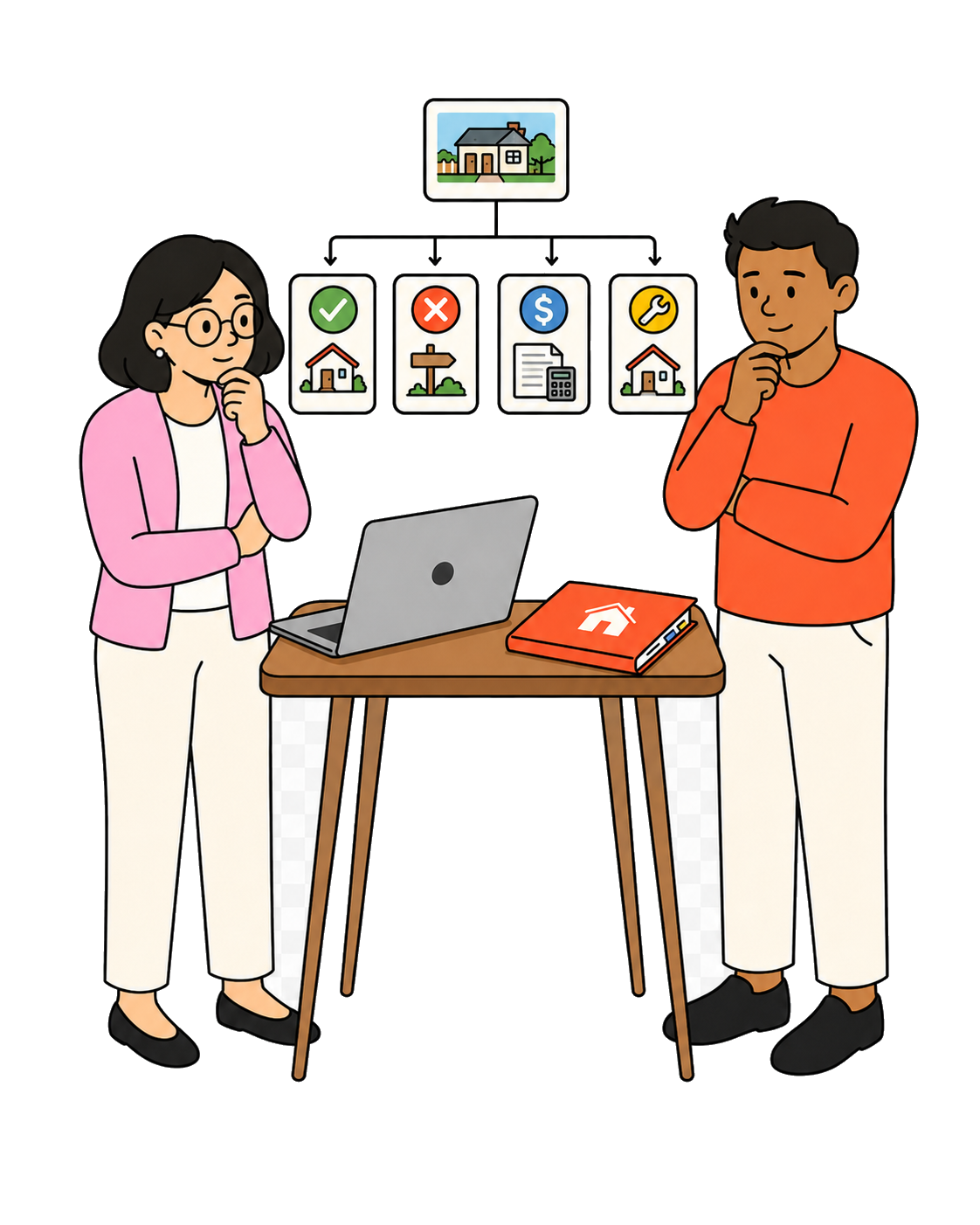

Each area exists to answer a different part of the same household-property problem.

Portfolios, members, loans, properties, living expenses, and goals stay connected.

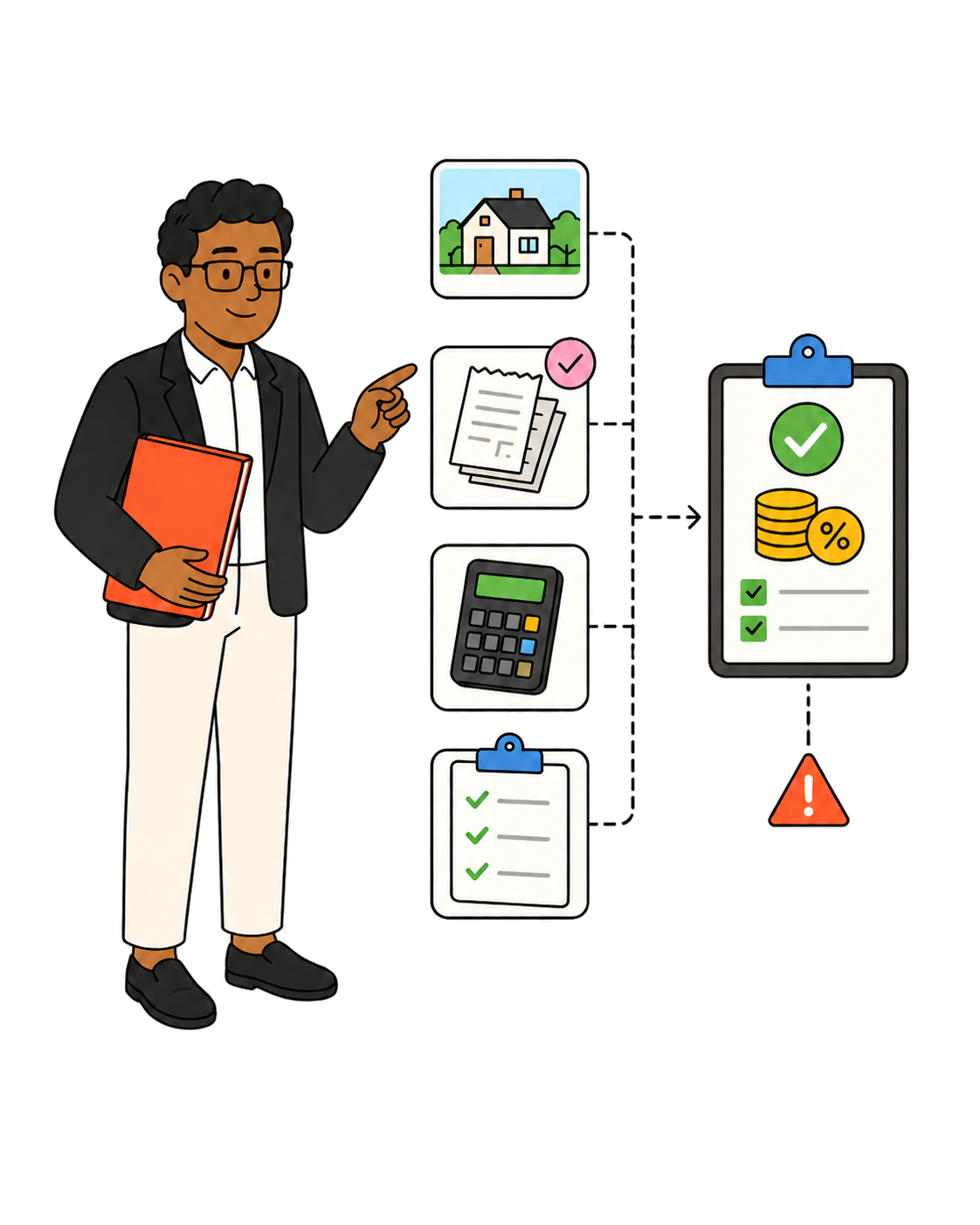

Current annual tax position, owner split, depreciation support, and sale audit trail stay visible together.

Search and compare suburbs by score, yield, growth, market phase, and peer context.

Read the current monthly position, then roll it forward under your own assumptions or a stressed case.

Compare keep, sell, and mixed retirement paths side by side using the current household and property base.

Create the portfolio, set up the records once, and move straight into the workflow that matters.